Leading global specialist risk consultancy, Control Risks (www.ControlRisks.com), and Oxford Economics Africa, announced the launch of the sixth edition of their Africa Risk-Reward Index today.

The Africa Risk-Reward Index is an authoritative guide for policymakers, business leaders and investors. The report monitors developments in the investment landscape in major African markets and delivers a grounded, longer-term outlook of key trends shaping investment in these economies.

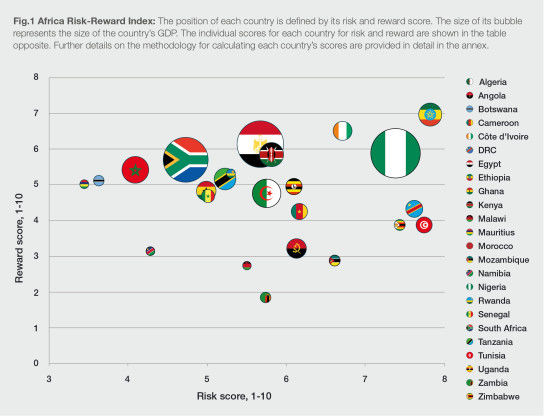

Africa is still in the midst of the COVID-19 pandemic, with vaccination rollouts progressing slowly and further waves of infections likely. This year’s risk-reward scores paint a picture of a continent recovering, albeit in an uneven and sometimes unpredictable way that raises as many challenges as it does opportunities. Reward scores have increased across the continent, in some cases substantially, but the risk scores show a more varied picture. The two do not always align; for example, the result of Zambia’s recent general elections is the driver behind a significant improvement in its risk score, but the country’s recovery remains hindered by an ongoing debt crisis.

This recovery is also occurring against the geopolitical backdrop of a recalibration of Africa’s relationship with the rest of the world. This 2021 edition of the Africa Risk-Reward Index explores this complicated landscape. We explain how government responses to three key issues (post-pandemic healthcare, debt, and insecurity) can accelerate or stall Africa’s economic recovery. The three articles explore these key issues in detail, flagging risk and opportunities emerging from these key trends. While the precise risks and rewards of any investment will vary greatly according to sector and project, this report is intended as a starting point for discussion, to help challenge preconceptions and set priorities for further exploration.

THE BIOTECH BOOM

COVID-19 highlighted a vulnerability in Africa that was caused by the continent’s reliance on external assistance when it comes to healthcare and biotech. Even as African governments reacted with often impressive speed to the pandemic, testing and treatment were constrained by a lack of capacity. Vaccine rollouts are progressing slowly due to supply constraints, as the rest of the world buys up large quantities of doses for domestic use. This article explores how these challenges have prompted new efforts to develop African capacity in the areas of healthcare and biotechnology and how these efforts are laying the foundation of what promises to be a hugely exciting industry.

“The global vaccine rollout has been extremely poor, with the unequal distribution of vaccines raising both moral and medical objections. Yet the one silver lining is that the challenges Africa has faced in obtaining not just vaccines but a whole range of equipment and treatments has spurred innovation and driven significant investments in African biotech and health-tech capacity. The emergence of an African biotech sector holds huge potential well beyond the COVID-19 pandemic and well beyond just healthcare applications,” says Barnaby Fletcher, Associate Director at Control Risks.

Genome sequencing capacity is currently being established in Liberia, Nigeria, Senegal and Sierra Leone. There are several initiatives to increase the continent’s ability to develop and manufacture vaccines, including an mRNA vaccine technology transfer hub in South Africa and manufacturing facilities in Egypt, Morocco and elsewhere. There has been a proliferation of laboratories, testing capacities and cross-border digital test and trace solutions. While these developments may have been driven by COVID-19, their application is not limited just to the current pandemic or even just to healthcare. The growth of a biotech industry in Africa holds huge opportunities for investors across the continent and in multiple sectors.

DECODING THE DEBT CRISIS IN AFRICA

Africa is facing a new debt crisis, with the continent’s combined debt-to-GDP ratio in 2020 reaching its highest level in two decades. Contained within this concerning overall picture lie even more worrying cases, such as Zambia, which became the first country to default on its debt during COVID-19 late last year. Africa’s debt burden was not fuelled by the COVID-19 pandemic but was exacerbated by it, and the cost of servicing it will divert fiscal resources that should be used to support the continent’s post-pandemic recovery.

According to François Conradie, Lead Political Economist at Oxford Economics Africa: “Africa’s debt burden has grown massively heavier over the past 18 months, as governments have borrowed to finance both their health response to Covid-19 and stimulus measures meant to lessen the pandemic’s economic impact. The current low interest rate environment makes the debt look manageable, but now the US Fed has made explicit that the countdown to tapering off monetary stimulus has begun. When central bankers worldwide start pushing up their rates, African governments will be faced with questions that have no easy answers.”

This debt burden poses risks for economies and companies alike. The obligation of servicing that debt will put strain on state-owned enterprises and will tend to limit opportunities for private-sector companies that do business with government. Options for restructuring or paying down this debt are limited, yet some innovative solutions are being discussed and tested. New social bonds and regional funding mechanisms will not offer a quick-fix substitute for sound fiscal management but can help reduce the threat such debts pose and offer new opportunities for investors.

IMPACT OF MILITARY INTERVENTION IN AFRICA

The US withdrawal from Afghanistan in August seemed to confirm a long-discussed idea: that the Western world no longer has the political appetite for foreign military interventions. This is as true in Africa as it is elsewhere. The US withdrew from Somalia in January, while France has announced plans to reduce its military presence in the Sahel. This is coming at a time when an upsurge in militancy and tensions in the Horn of Africa arguably make the continent’s security environment more volatile than it has been in decades.

In the absence of foreign military interventions, what new approaches are taken to address these security threats will shape the continent’s security landscape. The next few years are likely to be unpredictable, with African and external actors trying new strategies. At best, these take the form of regional cooperation, such as that seen in The Southern Africa Development Community (SADC’s) intervention in Mozambique, or even complete reassessments of how to tackle militancy. At worst, unilateral actions will escalate tensions as countries seek to establish themselves as security powers, driving – by way of example – the current arms race between Morocco and Algeria. This article unveils the changing dynamics of military assistance in Africa and examines what these mean for the security environment in which investors must operate.

Methodology

The Africa Risk-Reward Index is defined by the combination of risk and reward scores, integrating economic and political risk analysis by Control Risks and Oxford Economics Africa.

Risk scores from each country originate from the Economic and Political Risk Evaluator (EPRE), while the reward scores incorporate medium-term economic growth forecasts, economic size, economic structure, and demographics.